7 consecutive Scudetti.

4 consecutive Coppe.

3 Supercoppe.

4 consecutive Domestic Doubles.

1 Domestic Treble.

We are a part of the most dominant era in the history of Italian football that started on May 19th in 2010 when Andrea Agnelli became the President of Juventus. One of his first actions involved the hiring of the remarkable Sampdoria duo, Giuseppe Marotta and Fabio Paratici.

Along with club legend Pavel Nedvěd, the Fantastic Four have taken the Torinese club to unimaginable heights. They have given stability and organisation in a long, well executed rejuvenating process.

14 domestic trophies in 7 years is an incredible achievement considering the club had gone trophy-less for 4-consecutive seasons. That is, out of 21-possible domestic trophies that could have been won since 2011/12, La Madama lost out on just 7, averaging a winning ratio of 2/3 trophies per year. Spectacular.

When you factor in 1 UCL quarter-final, 1 UEL semi-final and 2 UCL finals, in the last 5-seasons alone, it demonstrates significant continental growth for a team that crashed out win-less in the group stages of UEL, 8-years ago.

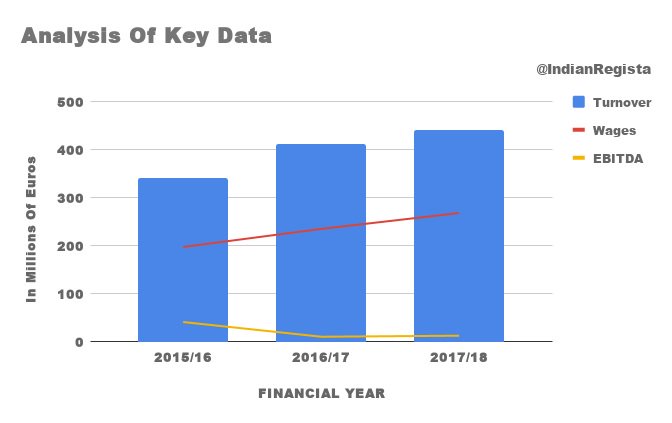

In the first financial year of the Andrea Agnelli leadership, the club recorded an operating loss of €92.2 million. In the seventh financial year, the club posted an operating profit of €67.4 million. A positive economic change of nearly €160 million in just 6-years despite the lack of commercial opportunities for Serie-A clubs. Extraordinary.

La Vecchia signora are now expected to record an operating loss of €9.8 million for the most recent season, the eight fiscal year of the new era overseen by President Agnelli.

Hence, the Piedmont club realizes that despite absolute domestic domination and important continental results, it is not enough for the club to maintain financial stability and still compete with the elite European clubs. The problem.

And voilà, Juventus make the coup of the century by securing Cristiano Ronaldo from Real Madrid. The solution.

In this three part series, I analyze the financial impact of signing CR7.

Part 1

Overview of current figures

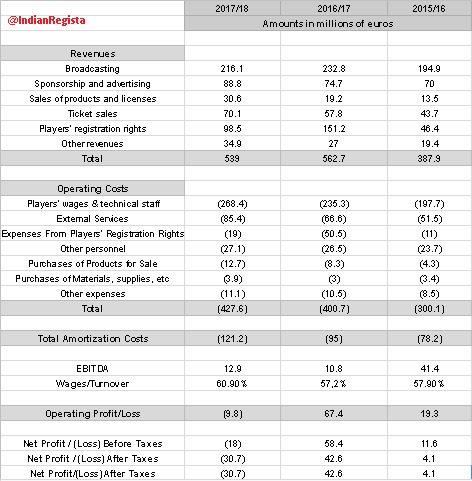

As highlighted in the aforementioned graphic, for 2017/18, the projected revenues are nearly €540 million while operating and amortization costs are nearly €428 million and €121 million respectively, resulting in an operating loss of around €9.8 million for the most recent financial year.

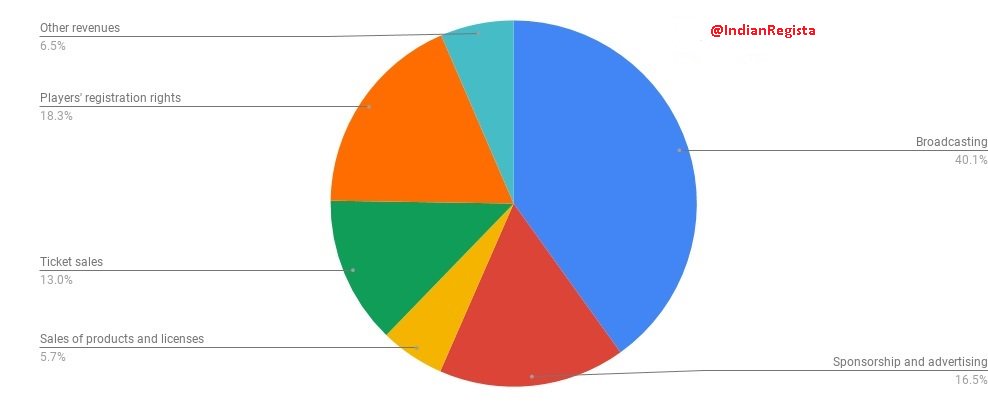

Revenue Division in 2017/18

There were positive revenue growths in revenues from ticket sales, sponsors/advertisers and products sales/licensing, in 2017/18 while compared to 2016/17. There was a +20% growth in ticket sales, mainly due to a hike in the price of seasonal and non-seasonal tickets. A growth of 18.8% was seen in sponsorship/advertising, as the club tied up with new domestic and international partners. An incredible growth of 60% in sale of products/licensing, was overseen, something that will be reasoned later in this report. Still, these positive increases are not comparable to the elite European clubs.

Notably so, Juventus are still highly dependent on competitive performances and important player sales to generate revenues. The money from UCL’s market pool is one of the main sources. A 7% drop in broadcasting revenues [nearly €16 million lesser] was mainly due to Juve’s exit in the UCL quarter-finals while Roma’s progression into the UCL semi-finals, causing the Turin based club not to maximize on the market pool. A 35% drop in revenues from player sales was expected as the club had sold Paul Pogba for a profit of over €70 million, in the previous fiscal year.

The operating costs continue to rise because the expenses on player wages and staff, are at an all-time high and there was a 14% increase. However, there was a 62% drop in expenses from players’ registration rights, which mainly consists of loan fees and costs incurred on FIFA agents for services.

The amortization costs also continue to rise. It increased by 28% due to an increased investment in the transfer market for remaining competitive on the pitch.

The EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is usually a good way to look at the performance of a business model. In this case, it corresponds to the difference between characteristic revenues or turnover [which is all revenues except revenues from player sales] and operating costs. The EBITDA increased by 20% , but it is still quite low at €12.9 million. The reason is because there is not enough growth in characteristic revenues to continue to support the rise in operating costs. Meanwhile, the wages to turnover ratio has increased to 60%.

FFP’s Break-even Requirement

The 2018 version of the Club Licensing and FFP regulations, states that:

“The acceptable deviation is €5 million but it can exceed up to €30 million if such an excess is entirely covered by contributions from equity participants and/or related parties.

The acceptable deviation is the maximum aggregate break-even deficit possible.

If the aggregate break-even result is positive (equal to zero or above) then the licensee has an aggregate break-even surplus for the monitoring period. If the aggregate break-even result is negative (below zero) then the licensee has an aggregate break-even deficit for the monitoring period.

The aggregate break-even result is the sum of break-even results of each reporting period covered by the monitoring period.

A monitoring period covers three consecutive reporting periods on which a licensee is assessed for the purpose of break-even requirement.”

In layman’s terms:

1. A club is considered not to have met the break-even requirement, if it records an aggregate operating loss of over €30 million for three consecutive financial years.

2. A club can be considered to have met the break-even requirement even if it records an aggregate operating loss of upto €30 million for three consecutive financial years, as long as the owners cover the losses.

So, when Juventus are monitored by UEFA’s Club Financial Control Body [CFCB] in 2018/19, this is what their balances will reflect:

2015/16 – €19.3 million operating profit +

2016/17 – €67.4 million operating profit +

2017/18 – €9.8 million operating loss –

Agg Result – €76.9m operating profit

Juventus have an aggregate break-even surplus of €76.9m when monitored by UEFA’s CFCB in 2018/19 for the reporting periods: 2015/16, 2016/17 and 2017/18. Hence Juve would be considered to have met the break-even requirement and be given a license to participate in UEFA competitions for the 2018/19 season regardless of their transfer activity in this summer and the forthcoming winter window.

Conclusion

The goal is to be financially sustainable without overly relying on important sporting performances. The objective is to compete with the elite European clubs without needing to make an important player sale. The growth of characteristic revenues lies locked within a door and Cristiano Ronaldo is the key to unlock the door.

References:

1. For the graphic pertaining to overview of figures in 2015/16 and 2016/17 financial year, I’ve taken the data from Juve’s official annual report.

2. For the graphic pertaining to overview of figures in 2017/18 financial year, I’ve taken the financial data from a report by Calcio & Finanza on 21 May 2018, making necessary adjustments to total amortization cost for the operations of Mattia Perin, João Cancelo and Douglas Costa.

3. Calculations of EBITDA and wages/turnover are my own.

4. Graphic pertaining to a comparison of top European clubs on revenues in 2016/17, is based on a report by Swiss Ramble.